Key Findings

Two years after the full implementation of the enhanced financial risk checks (EFRC) outlined in the government white paper enforced by Gambling Commission it is forecast:

EFRCs will have been requested on 4% to 6% of betting accounts that make up between 70% and 90% of gross gambling yield from online betting on horse racing.

Total contribution by gamblers through gambling operators to racing (through levy, sponsorship, advertising and supporting television) will drop by between £147m to £321m a year.

The racing levy will drop by £24m to £53m a year.

Prize money will drop by 14% to 32%.

Full Report

1. Introduction

In this paper we examine the implications of the Enhanced Financial Risk Checks (EFRCs) outlined in the Government White Paper on the future finances of British Racing.

The white paper suggested that operators are required to ask customers for EFRCs if they lose £1,000 in a day or £2,000 over a rolling 90 day period.

We examine the funding of British Racing and look at how gamblers currently gamble on the sport. We then assess what percentage of racing’s revenue is likely to be affected by the EFRCs and how likely gamblers are to comply with them. Finally we estimate the overall loss of racing’s revenue due to the checks.

We conclude that without any policy change the impact will be a 24% to 53% fall in the Levy and £147m-£321m drop in total revenue over the first two years. This will grow greater in the following years as more accounts are caught up in the EFRCs and the interest by gamblers, owners and racing fans in the sports inevitably declines.

2. Background on the Finances of Horse Racing in Great Britain

According to the British Racing Authority, British racing contributes £4.1bn to the British economy.

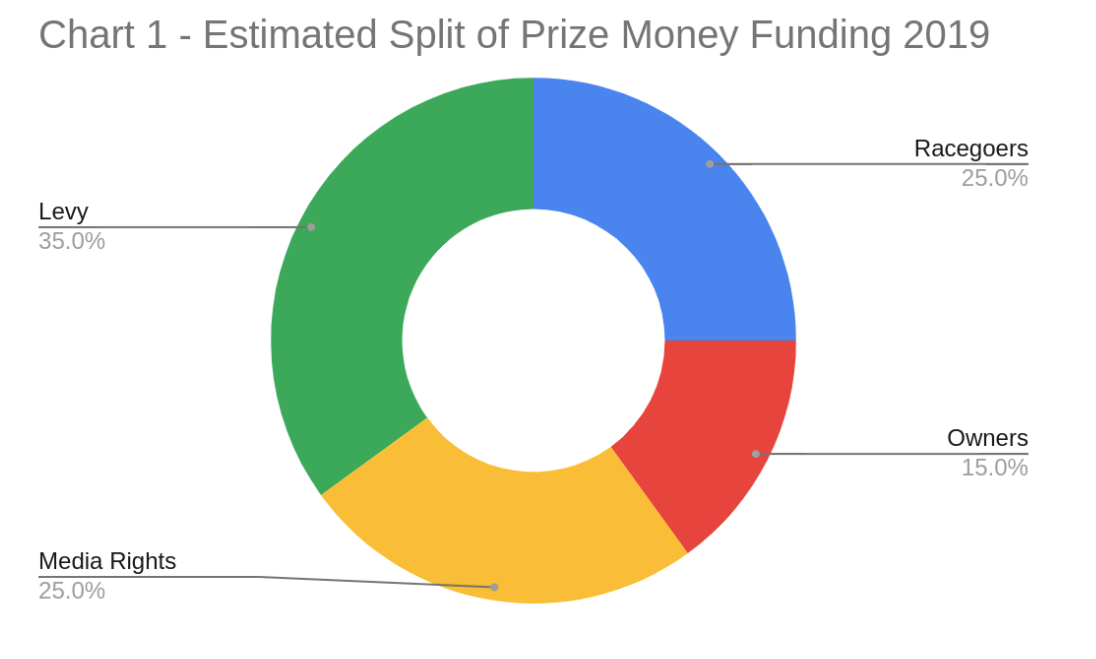

In 2019 British racing had a number of different income streams that included owners (over £600m), breeding (£330m), racegoers (£260m), media rights (£150m), levy (£95m) and sponsorship (£50m).

2.1. Prize Money

The total prize money in 2021 was £148m. This was down from £161m in 2019. In 2020 and 2021 the Horse Racing Levy Board (HRLB) drew on its reserves and financed 62% and 51% of prize money respectively. Going back to 2019 the breakdown of prize money funding was 50% racecourses, 15% by owners and 35% by the HRLB. We allocate 50% of the racecourse contribution to media rights and sponsorship.

2.2. Betting Companies

In 2022/23 Betting and Gaming Council members (85% of GB betting) contributed £384 directly to British Racing in levy, media rights and sponsorship. They also spent £125m on marketing to promote racing and betting, helping to secure terrestrial TV coverage and support two specialist racing channels. If we assume the other 15% of betting operators spent similar amounts the total contribution into racing and its promotion was £599m.

2. Background on the Finances of Horse Racing in Great Britain

The Gambling Commission have collected turnover and gross gambling yield (GGY) data on horse racing bets struck with operators licenced by them since April 2008. The data in this section is collected from their website.

The data is split between non-remote (over the counter, pools and on course) and remote. The Gambling Commission only started collecting remote data in November 2014 after the new licensing laws came in. The first full year's data started in April 2015. The data includes British and foreign racing. British racing accounts for 80%-85% of GGY.

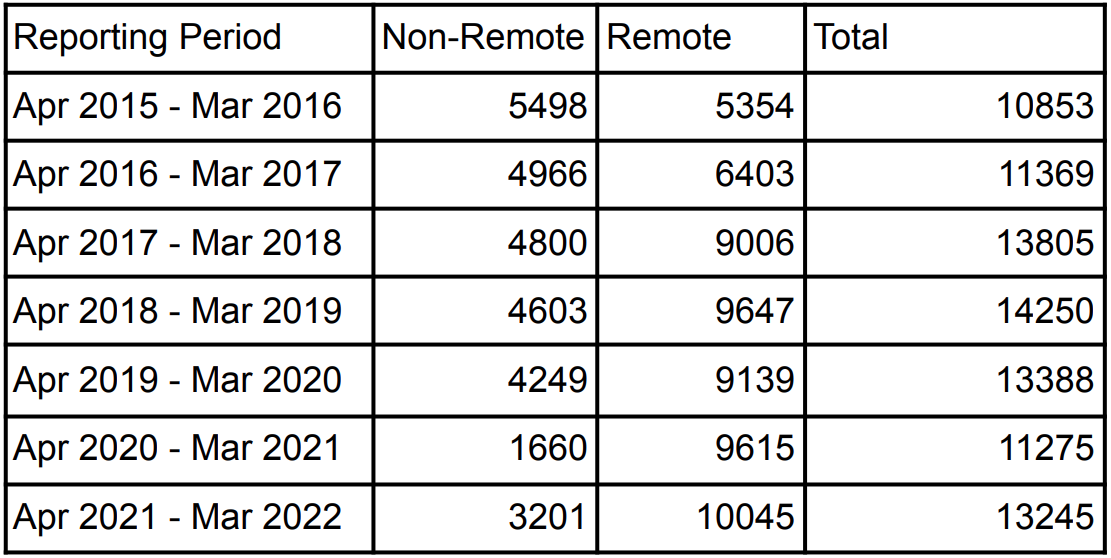

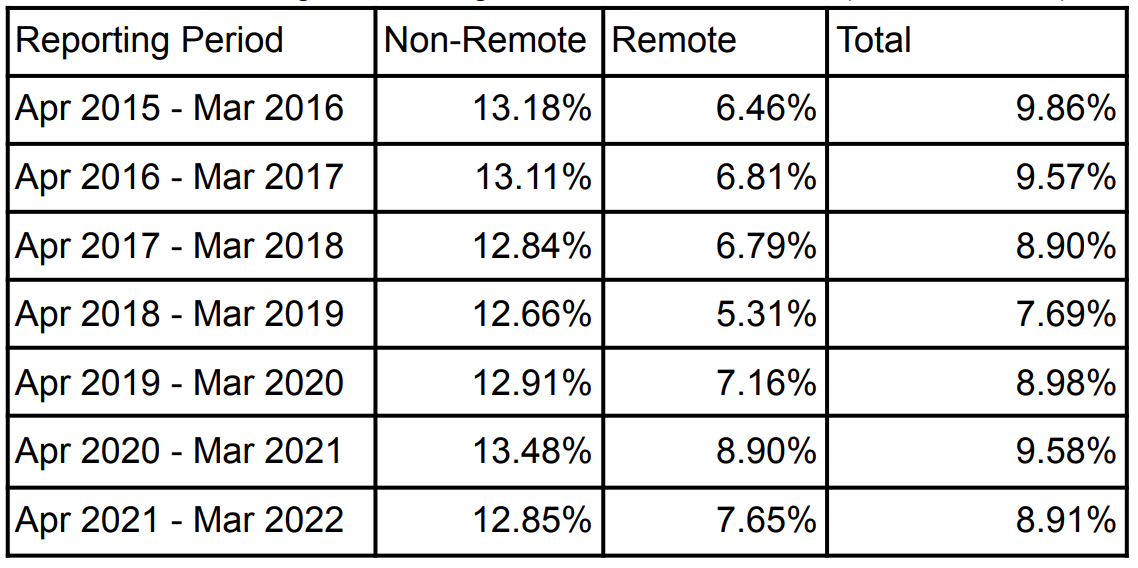

Table 1 - Turnover on Racing non-remote and remote (£m)

Table 1 shows that in 2015/16 turnover was equal betting cash and remote. Overall turnover peaked at £14.2bn in 2018/19. By 2021/22 remote was 3 times the size of non-remote.

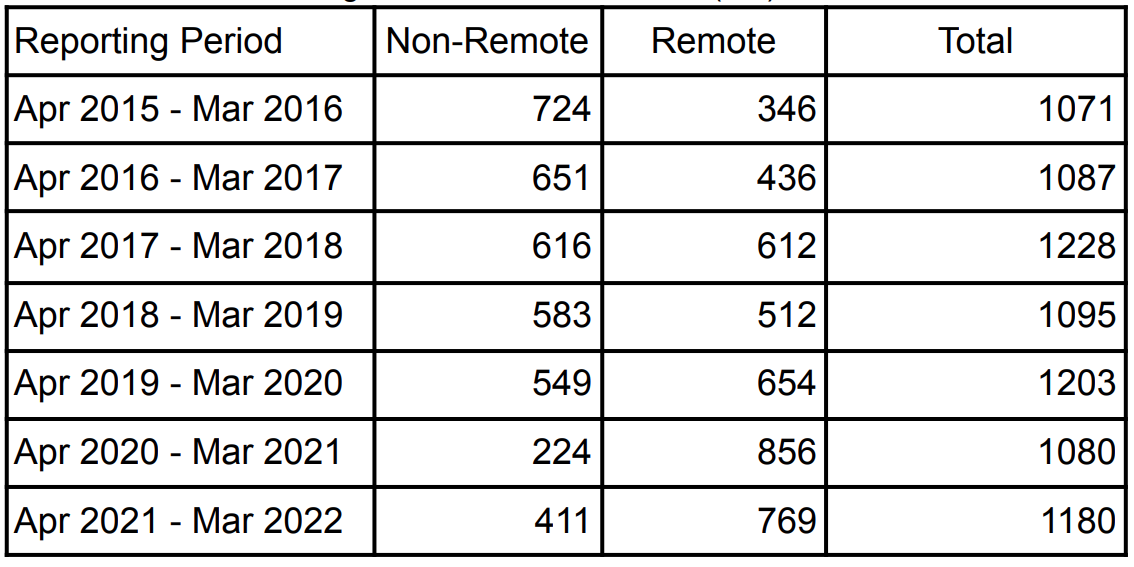

Table 2 - GGY on Racing non-remote and remote (£m)

Total GGY from both channels peaked in nominal levels of £1.23bn in 2017/18. In 2021/2022 they were back up to £11.8bn after dropping during the Covid lockdown when betting shops were closed (they reopened in April 2021). Given that foreign racing accounts for 15-20% of the CGY it can be estimated that CGY from British racing from non-remote and remote settings is around £1bn a year.

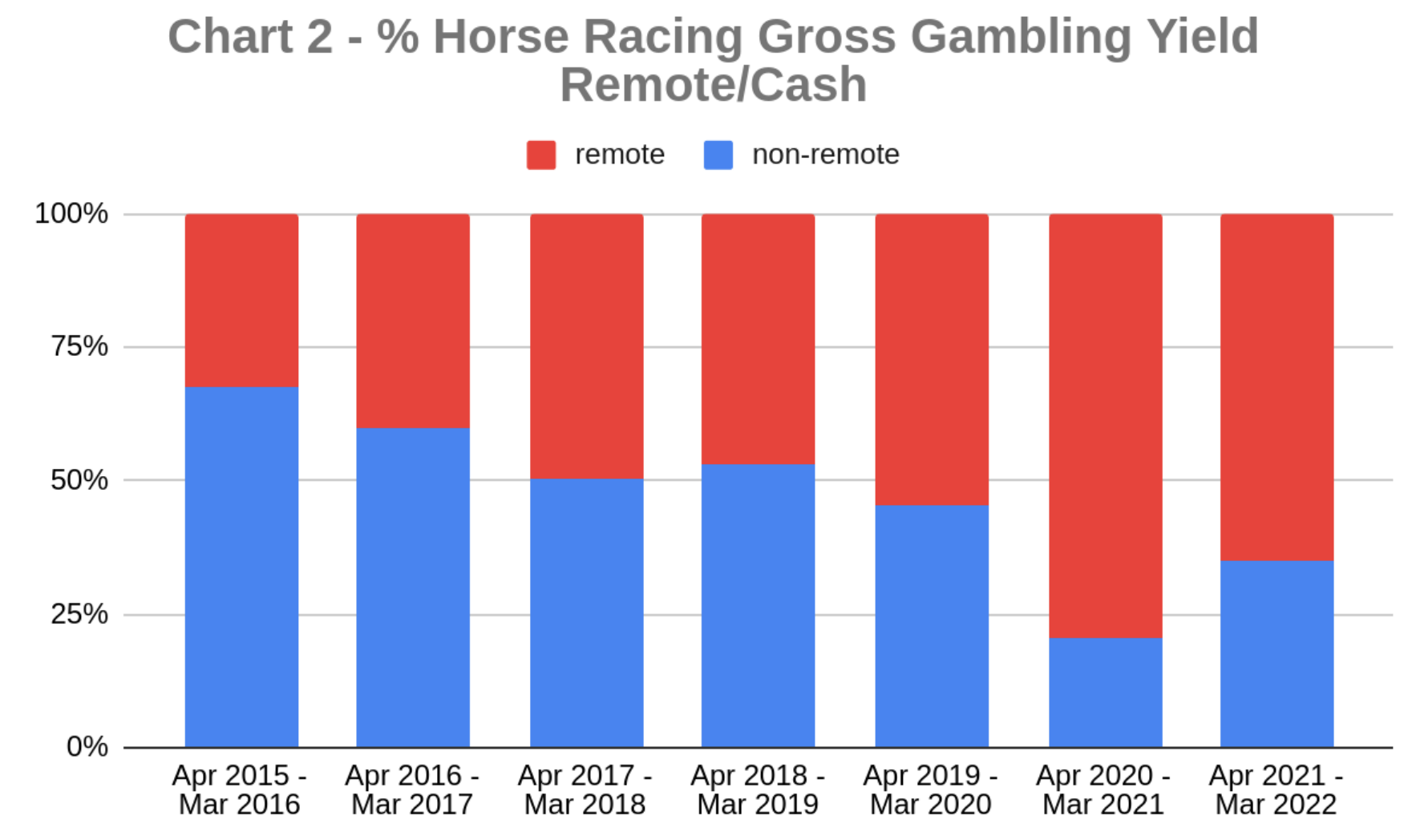

Chart 2 shows how the percentage of GGY has switched from remote to non-remote channels between 2015 and 2022. Non-Remote represented 68% in 2015/2016 but was down to just over 30% in 2021/22. The lower number for 2020/21 can be attributed to Covid lockdown but the trend looks set to continue. The number of betting shops dropped from 8304 in 2018/19 to 6219 in 2021/22.

The betting exchanges saw a 23% fall in their GGY from £161m in 2019/20 to £124m in 2021/22. This should be noted because exchange customers are likely to be bigger gamblers (more active, more turnover) and thus are more likely to have already been forced into the current affordability checks.

Table 3 - Gross Margin on Racing non-remote and remote (GGY/Turnover)

Table 3 shows the gross margin betting operators made on racing. Non-remote levels are relatively stable but margins on remote betting are edging up.

4. The Proposals in the Gambling White Paper and Gambling Commission Consultation

The Department for Culture, Media and Sport published its White Paper ‘High Stakes: Gambling Reform for the Digital Age’ in April 2023.

The paper stated that they wanted ‘obligations on operators to conduct checks to understand if a customer’s gambling is likely to be unaffordable and harmful.’

The proposal was for two types of ‘financial risk’ checks:

- Background checks for a loss of £125 in a month or £500 in a year. They would check for financial vulnerabilities such as CCJs.

- Enhanced checks at £1,000 net loss in a day (‘binge gambling’) or £2,000 net loss over 90 days (‘sustained losses over time’).

The values are halved for customers aged 18 to 24.

The paper made several further comments:

- The enhanced checks would only affect 3% of online gambling accounts.

- Intention for checks to be frictionless through open banking and/or credit reference agencies.

- Further information should only be requested as a last resort.

- Where there are serious concerns operators should share information.

- ‘..it is not the intent that government or the Gambling Commission should set a blanket rule on how much of their income adults should be able to spend on gambling.’

The Gambling Commission published its consultation document containing the financial risk checks in July 2023.

The background credit checks proposed are the same as the White Paper for £500 a year or £125 in a month losses.

For ‘binge gambling’ additional detail was added that a positive net position for the last 7 days could be taken into account. This means that if a gambler is on a good run in the last week they can gamble beyond the £1,000 loss limit for a day without checks. But beyond the 7 days previous wins are excluded from calculations. These checks would need to be repeated in six months if the £1,000 daily threshold is reached again.

The ‘sustained losses over time’ checks are required if £2,000 is lost in a rolling 90 day period. These checks would also need to be repeated in six months if the £2,000 90 day threshold is reached again.

For the £1,000 and £2,000 checks, lifetime position of the account may not be taken into account or winnings from another operator when deciding to do a check.

Bets staked only contribute to the checks once they are settled as a loser.

The proposals state for £1,000 and £2,000 checks licensees must obtain credit performance data and; income and expenditure, including current account turnover data. Using this information and other information they know about the client they must manually make a decision to take proportionate action if risk is identified. The long term position of the account can be taken into account at this stage.

The Gambling Commission estimated 3.2% of betting accounts (1,000,000 accounts) would need an enhanced assessment for the £2,000 losses in 90 days. They also stated 2% of accounts would need to be assessed for 1 day losses of £1,000. It is important to note that many of the same accounts are going to cross both thresholds.

5. Modelling and Analysis of the Financial Risk Checks on Different Customer Types

The report ‘Potential Impact of Enhanced Financial Risk Checks on Different Types of Gamblers’ has all the calculations for this section.

5.1. Initial observations

Gamblers who stake under £1,000 every day and under £2,000 every rolling 90 days in their betting accounts should never face enhanced checks. This means, in theory, a gambler could lose just under £8,000 in any rolling year and not have an enhanced financial risk check request.

Higher staking gamblers are under the constant threat of checks due to randomness of results. Depending on their style of gambling this threat may be greater or smaller.

5.2. Customer Types

This section provides an insight into how different customer types are likely to be affected by the Enhanced Financial Risk Checks (EFRC).

Gambler 1 is a racehorse owner. He likes to bet £1,000 on his own horses twice a year at 5/1.

Gambler 2 loves to bet on racing accumulators dreaming of a big win. Every day she bets £10 on two 4 horse accumulators. The accas are priced at 10,000/1.

Gambler 3 is a racing enthusiast. He likes to place two win single bets a day of £25 on his best selections. They are always priced at 8/1.

Gambler 4 is a serious form student. She is extremely selective with her selections betting £500 once every 2 weeks with a win single on an even money shot.

Gambler 5 enjoys playing roulette. Everyday he bets £1 on 500 spins on red at even money.

The five customer types were run through simulation code. The full assumptions and calculations are in the appendix. Each cohort was given 10,000 ‘customers accounts’ running the simulations 10,000 times.

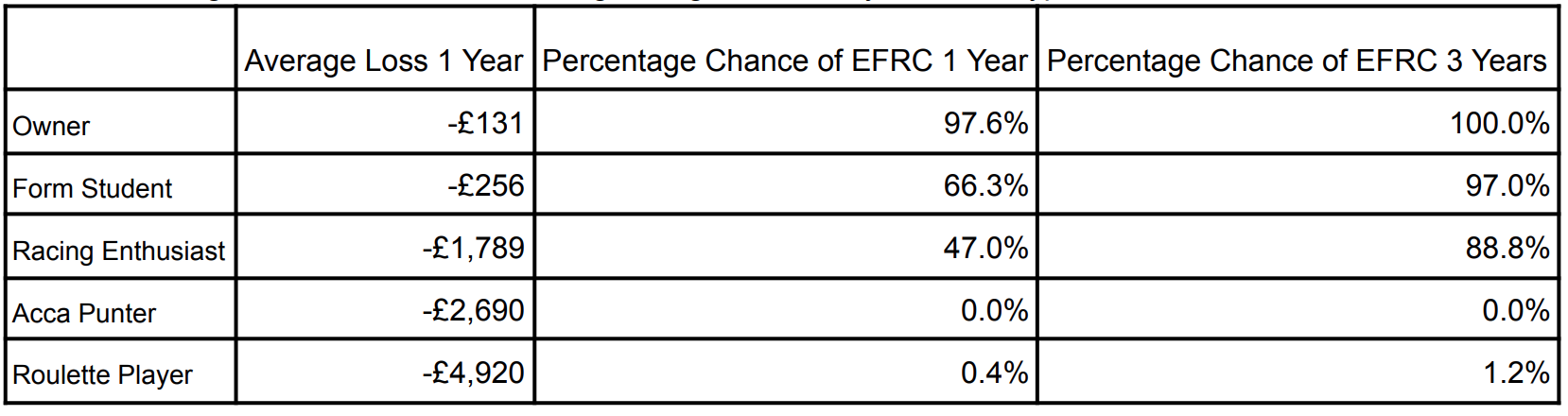

Table 4 - Average Profit and Chance of Being asking for EFRC by Gambler Type

In this example the owners have the lowest annual average annual loss of £131. 98% of these owners will have been asked for an EFRC within the first year. This is due to the request to have a £1,000 bet and that being regarded as a binge gamble if the bet loses.

The Form Student has an average loss of £256 and a 66% chance of being asked for an EFRC in year 1 up to 97% by the end of year 3. The Racing Enthusiast placing 2 £25 win singles a day is next with an 89% chance of being asked for an EFRC within 3 years.

The Acca Punter and Roulette Player have the biggest average losses. They are also both extremely unlikely to be asked for an EFRC. The Acca Punter only stakes £20 a day (£1800 in 90 days) keeping her under the £2,000 threshold at all times meaning no EFRC requests. The Roulette Player stakes £500 a day (£18000 in 90 days) but bets with high frequency and low average stakes keeping his betting variance over 90 days very low. It is just steady losses for him through time resulting in an average loss of £4920 over the year.

6. Analysis of online horse racing accounts through empirical evidence

6.1. How many accounts will have an EFRC request?

The assertion by the Gambling Commission that 3.2% of gambling accounts will be asked for an EFRC for losing £2,000 in a rolling 90 days was from a survey of 5.86 million active accounts in a time period from May 2020 to April 2021. The same survey found that 2% of accounts lose £1,000 in a 24 hour period. These accounts included sports betting, betting on racing and casino games.

The £1,000 loss in a 24 hours period data collected does not account for the new proposal that wins within 7 days could be offset against the daily loss. This should reduce the number of accounts required for an EFRC. Accounts may qualify for both checks so we cannot add 2% to 3.2% to work out the total number of accounts.

The EFRCs are due to start in summer 2024 and the above data was collected in 2020/21. The Bank of England Inflation calculator was used to convert 2020 values to July 2023 and 5% was added to take us to summer 2024. The overall inflation results in £2,000 when the data was collected increasing to £2528 when the policy is due to be implemented.

If the thresholds are not increased by implementation around 4.1% of accounts will breach the £2,000 threshold and 2.5% accounts will hit the £1,000 in a day threshold. Accounts may qualify for both checks so we cannot add 4.1% to 2.5% to work out the total number of accounts affected in the first year.

This number is the total number of active accounts for all remote betting and gaming. We know from the calculations in previous sections that certain types of betting are more likely to be checked than others. We also know that the process is not stationary for a year. Accounts that avoid checks in year 1 can breach a threshold in the following years.

Taking all the parameters into account it is estimated that between 4% and 6% of accounts that bet online on British Racing will be subject to an EFRC request within 2 years of their implementation.

6.2. What percentage of online GGY for horse racing will be affected by EFRC?

The University of Liverpool carried out a ‘Patterns of Play’ study into online gambling. They studied 140,000 betting account data from 7 operators from July 2018 to 30th June 2019. This data gives us an insight into the GB online gambling market at the time.

A report to Gamble Aware using this data concluded that:

‘the 5% of accounts with the highest spending generated 86% of GGY.’

This applied to the betting elements of all the accounts. Unfortunately the statistic was not applied just to horse racing bets.

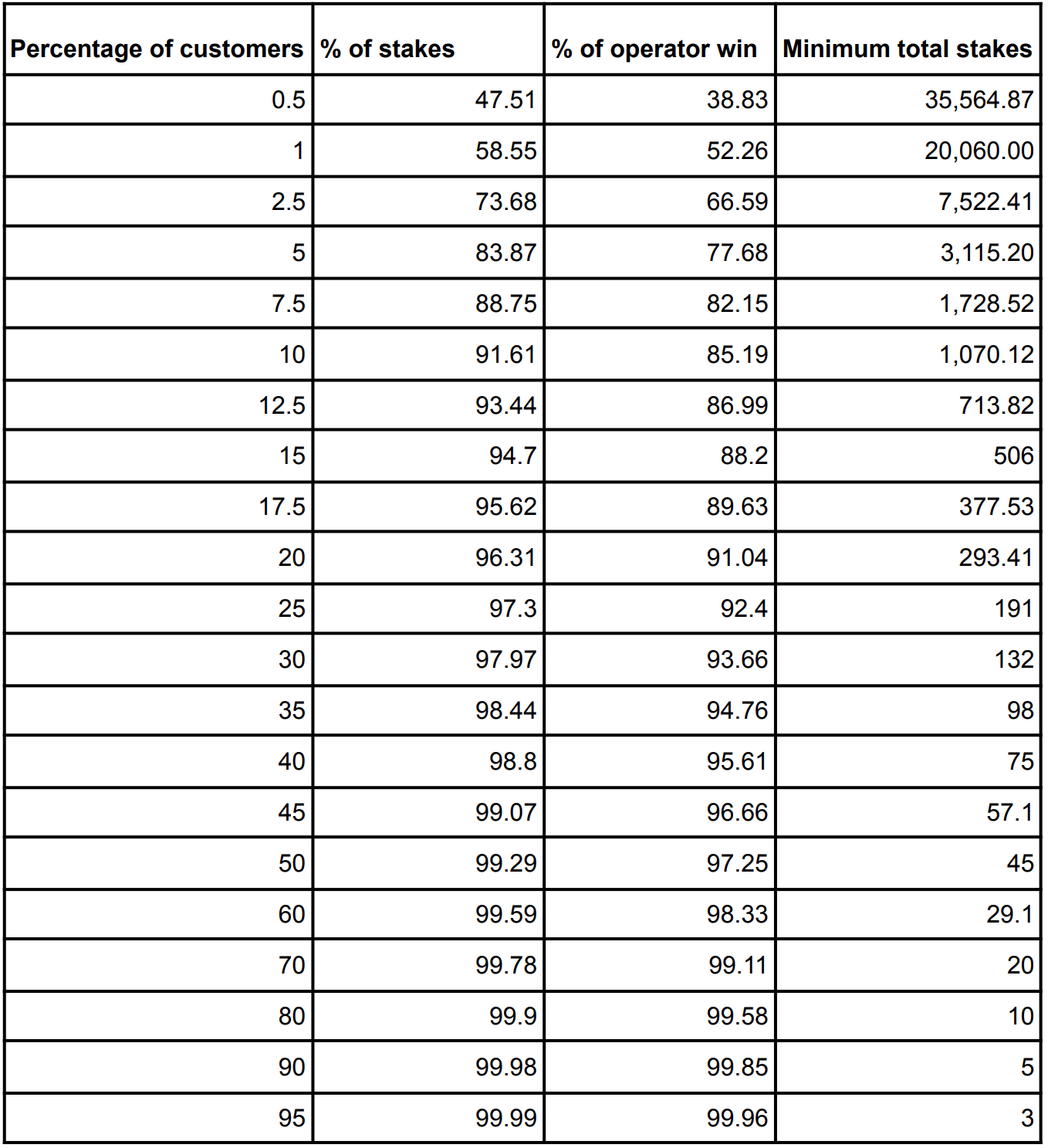

Table 5 - Horse Racing Bets accounts by total staked

Table 5, from the Patterns of Play data, shows the split of percentage of total stakes and operator win by ordering the customer accounts by total staked. For instance, the top 5% of customers by total staked made 74% of the total staked by all customers and contributed 67% of operator win (GGY).

From the analysis in the previous section we know that total stakes and total loss in a year cannot tell us precisely which accounts will be subject to EFRC requests. It should also be noted that the data in Table 5 only applies to the horse racing element of active accounts. The same accounts could also have lost (or won) money betting on other markets and in the casino.

We take our estimate that 4%-6% of horse racing accounts will be asked for checks as a starting point. The fact that 5% of accounts contribute 86% of GGY is also taken into account. Anyone staking over £8,000 a year is very likely to be checked at some point through random results.

It is estimated that between 70% and 90% of online horse racing GGY is linked to accounts that will be asked for a EFRC within 2 years of the implementation.

7. How many gamblers will comply with and pass an EFRC?

The Gambling Commission stated in the consultation that income and expenditure, including current account turnover data should be used for the EFRC. In order to obtain this information on each customer the operator will need access to banking information either through physical bank statements or open banking. If the bank statements do not provide enough information to make a decision, extra information can be requested. This would apply to be people with limited standard income but saved wealth, their own businesses and pension funds.

7.1. Implications for betting operators

Potentially 2 million betting accounts will require EFRCs to continue betting. Managing this, even with open banking assistance, is going to be a big task. The Gambling Commission has said that the final decision for each account must be made manually. Time and resources might be better spent just closing accounts and refocusing on high frequency/low stake (slots, roulette) and multiplies betting (accumulators and Bet Builders) that will generate steady income and be less likely to be subject to EFRC requests. Operators are also likely to be over cautious due to the continuous threat of Gambling Commission fines.

7.2. Implications for gambling consumers

Once a gambler hits a threshold he or she will be asked by the betting operator for a EFRC check. Although producing physical bank statements requires more effort than allowing open bank access both options amount to the same result. Gamblers will be required to give operators access to their private financial information in order to bet with their own money. If a gambler is losing money it is hard to see the motivation to give up the information. It is different from obtaining a mortgage or loan where the person allowing open banking access is borrowing money.

If the gambler refuses to provide the information his account with that operator will be closed. If the gambler does comply he may fail the checks and still not be allowed to bet his or her own money in the amounts desired.

7.3. Why will gamblers refuse to comply?

7.3.1. The information is private

Many gamblers might see it as an invasion of privacy to give a gambling company access to their private banking and financial history. It is different from applying for a loan when the applicant has to prove they can pay the loan back. These checks are for someone to assess how much of the gambler’s own money they can spend.

7.3.2. They would fail the test or it is too complicated

Some gamblers may not have a standard income that could justify betting the levels they want to bet through regular income. They might happily set aside several thousand pounds of their own money as a betting bank separate from their daily expenses but the EFRC system would not allow for it. They might have a pension pot, other investments, property or irregular income from their own business. All these things make assessing if they have the disposable income they want to bet very difficult.

7.3.3. They do not trust the betting operator with intrusive information

GB regulated bookmakers have been fined tens of millions of pounds for regulatory failings in recent years.William Hill Group received a record £19.2m fine in March 2023.

Cracked Labs conducted a study in 2022 that found extensive digital profiling in the online gambling industry. Although information collected for EFRCs is not supposed to be used for commercial purposes it is hard to see how that could be avoided. For instance, just knowing a customer has a £20,000 deposit limit indicates to the marketing department that the customer is worth a big marketing spend. Information in bank statements showing winnings from other operators could also be used to limit customers. In 2018 the CEO of Skybet admitted 1% of their customers were limited to winning £100 a bet.

6,000 complaints a year also go to the Gambling Commission with customers have delays or blocks on the withdrawal of funds. There is a danger that operators could use the access of banking information for EFRC and source of funds checks to block withdrawals and/or limit betting accounts. Given the adversarial relationship between gambler and operator it is questionable whether operators themselves should have access to private banking data under any circumstances.

7.3.4. Option of other GB licensed operators

If one operator closes an account the gambler could move to another with a GB licence. In time they will eventually run out of operators but this could keep a moderate gambler betting for a while.

7.3.5. Option of non-GB licensed operators

Prior to the Gambling (Licensing and Advertising) Act 2014 most British gamblers who bet remotely did so with operators not licensed in Great Britain. This state of affairs essentially started when Victor Chandler moved to Gibraltar in 1998. Prior to this British gamblers had to pay 9% on turnover tax on all off course bets.

Since 2014 all operators targeting Britain should have a GB licence. Currently the rate of betting by British residents with operators not licenced here is estimated to be around 1% of turnover. However, as the ERFC regulations begin to exclude British punters from the GB licenced market this is likely to grow. British gamblers have demonstrated historically they are comfortable betting with non GB licensed firms. Increasing regulation is likely to cause more betting with non-local licensed operations. For instance in Norway, where higher risk games have a monthly lose limit of 517 euros a month, a PWC report found 66% of money staked was not with Norwegian licensed operators.

7.4. Compliance estimates

A survey in the Racing Post found that 85% of customers would not be willing to provide operators with bank statements. Martin Burt from open banking firm Clear Stake estimated that 70% to 80% would refuse to provide physical bank statements. He suggested people were willing to use open banking in renting and mortgages. But the key difference is those checks are for credit to borrow money or sign a lease that might not be paid in future. The ERFCs are checks for consumers to spend their own money. Tom Farrell, also from Clear Stake suggested that getting compliance down from 85% to 80% would be a result for some operators.

It is estimated that between 50% and 85% of customers asked for banking statements and/or open banking access for EFRC checks will refuse.

8. Implications for horse racing’s finances

Gross Gambling Yield from British horse racing bets is around £1bn a year with £700m of that coming from the remote sector that is to be subject to the ERFCs.

It is estimated that GCY for GB racing accounts required to carry out EFRCs within 2 years is £490m-£630m. This is calculated from the estimates that between 70% and 90% of online horse racing GGY is linked to accounts that will be asked for a EFRC within 2 years of the implementation.

It is estimated that GCY for GB racing accounts loss due to refusal/failing checks within 2 years will be £245m-£535m. This is calculated by using the 50% to 85% of customers who will refuse to comply with or fail EFRC checks.

Reduction in levy 24% to 53% (£24m-£53m). This assumes a levy of 10% of GGY from British racing.

Reduction in total betting operator contribution to racing £147m-£321m. This is calculated from the assumption that 60% of operator GGY from British racing bets comes back to racing in levy, sponsorship, media rights, marketing and promotion.

Reduction in prize money (if owners and racegoers contribution remains same) will be 14%-32%. This is calculated by the assumption that 60% of prize money comes from media rights and the levy.

9. Discussion and Conclusions

Racing and betting have been intertwined since the sport was first introduced. A 24% to 53% drop in the gross gambling yield that betting operators make from racing bets following the introduction of the EFRCs is likely to have a catastrophic effect on the racing industry within 2 years of its introduction.

The analysis in this paper has not accounted for how owners might react to EFRCs and not being able to bet on their own horses to any reasonable level. Leading owner Carl Hinchy announced in August 2023 that he was quitting being an owner due to the checks. Owners currently contribute over £400m a year to the sport (costs - returned prize money). If they quit in larger numbers this will further compound the problems of British racing.

Potential EFRCs in future for non-remote betting are also not accounted for in this paper. Remote betting is an easy target for the checks because all the information is digitised. In New South Wales, Australia, cashless gambling is being trialled. In Victoria cashless gaming cards will be mandatory. Operators in the UK are bringing these checks in for source of funds and affordability. With 30% of racing GGY coming from the non-remote sector any wholesale checks there would further damage British racing.

The consequences of the EFRCs are likely to be an increase in the number of low stake high margin accumulator bets and low stake high frequency bets. The gambling operators are likely to focus on these products for racing, sports and casino betting. The incentive for operators to offer higher stake, low margin bets has fallen due to extra cost of processing EFRCs for those types of bets and the threat of action from the regulator.

Unlinked to EFRCs the margin for horse racing bets is already rising with winning gamblers being shut out of betting as operators restrict their stakes. The Skybet number of 1% of accounts being restricted to winning just £100 highlights this. Given that many accounts have very few bets a year the 1% could represent a lot of low margin turnover lost. Although mentioned in the Gambling White Paper, neither the Gambling Commission or the DCMS suggested curbing this practice. In Australia most states make betting operators lay horses to lose at a minimum of $2,000 (c. £1,000) on metro racing to any gambler. Ironically an even money bet at this level would be regarded as ‘binge gambling’ in Britain.

The collapse of gross gambling yield on the betting exchanges is a warning of things to come. They are likely to attract higher staking lower margin gamblers that are restricted with traditional bookmakers. This cohort of gamblers are therefore more likely to have already been asked for affordability information. Leading gambler and racing author Alan Potts announced in August 2023 he was quitting Betfair due to affordability checks. The decline of betting exchanges, EFRC checks and other restrictions by traditional bookmakers leave larger staking and more skilled gamblers nowhere to bet on racing other than non-GB licensed operators.

If racegoers, gamblers and race fans face a restriction on their ability to choose how much of their own money they can bet, many will choose to bet with non-British licensed firms. Although these firms will not be able to advertise in Britain or pay into the levy they could provide a lifeline to the sport in keeping owners and gamblers' interest alive in racing. This could potentially limit the drop in demand for owners, racing TV subscription channels and media.

There is no doubt that any type of affordability checks will be devastating for British Racing. The levy will drop dramatically and replacing it with a turnover system will be even worse as operators are moving to a high margin lower turnover model. But the levy is only a small proportion of gamblers’ losses on British racing bets that finds its way back into the sport through betting operators. They contribute almost 6 times the value of the levy when media rights, sponsorship, marketing and promotion is taken into account. All of that is under threat by Enhanced Financial Risk Checks.